Nebius Supercloud: 2026 Bull vs. Bear Verdict

The artificial intelligence infrastructure sector in 2026 has moved far beyond early hype cycles and speculative valuation models. It is now defined by large-scale capital deployment, power-constrained expansion, and long-term enterprise contracts that shape global compute availability. Within this evolving landscape, Nebius Group NV (NASDAQ: NBIS) has emerged as one of the most closely watched “neocloud” operators, positioned at the intersection of GPU supply, data center expansion, and hyperscaler demand.

As of mid-2026, Nebius is no longer viewed as an experimental cloud provider. Instead, it is increasingly analyzed as a structural proxy for AI infrastructure capacity itself. However, this transformation brings both opportunity and risk, creating a sharply divided bull and bear debate centered on execution, capital intensity, and long-term customer dependence.

Scaling into AI Infrastructure Demand

The defining feature of Nebius’ current phase is rapid operational scaling driven by enterprise AI demand. The company’s AI cloud segment now represents the overwhelming majority of its revenue base, reflecting its pivot away from traditional hosting toward GPU-intensive workloads.

In Q1 2026, Nebius reported revenue of approximately $399 million, reflecting extremely high year-over-year growth driven by expansion in AI compute contracts and accelerated GPU deployment cycles. While such growth rates are typical in early-stage scaling environments, sustaining them requires continuous infrastructure expansion and strong customer retention.

A key driver of this expansion is the company’s long-term contractual pipeline with hyperscale customers. Among the most significant is a multi-year capacity agreement with Meta Platforms, reportedly valued at up to $27 billion over time. This agreement, along with additional phased capacity arrangements with Microsoft, provides Nebius with visibility into future demand while also tying its business model closely to a small number of large enterprise clients.

However, while these agreements provide demand certainty, they also introduce concentration risk. A significant portion of Nebius’ future revenue trajectory is indirectly linked to hyperscaler AI strategies, which remain fluid and subject to internal infrastructure development cycles.

The Power and CapEx Arms Race

The most important constraint in AI infrastructure today is not demand—it is physical capacity. Power availability, grid interconnection timelines, and data center construction cycles now define competitive advantage more than software differentiation alone.

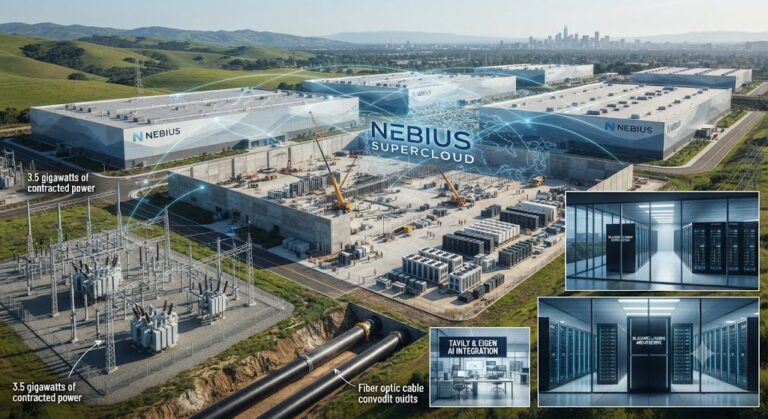

Nebius has responded by aggressively scaling its infrastructure footprint. The company has secured more than 3.5 gigawatts (GW) of contracted power capacity, with targets exceeding 4 GW by year-end. This includes large-scale developments such as its Pennsylvania AI-focused campus and additional expansion projects in the U.S. Midwest.

To support this buildout, management has significantly increased capital expenditure guidance for 2026, raising projections into the $20 billion–$25 billion range. This marks a clear shift from a growth-at-scale strategy to a capital-intensive infrastructure race aimed at securing long-term positioning in the AI compute supply chain.

While this level of investment enables Nebius to lock in scarce resources such as power and GPU clusters, it also introduces substantial execution risk. Large-scale data center projects are highly sensitive to delays in permitting, grid connectivity, and equipment deployment, all of which can impact both timelines and profitability.

Financial Position and Liquidity Strength

A key pillar supporting Nebius’ expansion strategy is its strengthened balance sheet. Following a combination of equity financing, convertible instruments, and strategic investment participation, the company reportedly maintains over $9 billion in liquidity.

This includes a notable $2 billion strategic investment from NVIDIA, which aligns Nebius more closely with the broader GPU supply ecosystem. This relationship is strategically important because access to next-generation GPUs, such as NVIDIA’s Blackwell and future Rubin architectures, is a critical determinant of competitive positioning in the AI cloud market.

The strong liquidity position provides Nebius with runway to execute its aggressive infrastructure expansion without immediate dependence on additional external financing. However, given the scale of projected capital expenditure, long-term funding sustainability remains a central investor consideration.

The Bull Case: Structural AI Utility

Supporters of Nebius argue that the company is transitioning into a foundational layer of global AI infrastructure. In this view, Nebius is not simply a cloud provider but a specialized utility for high-performance compute.

The bull case rests on three pillars.

First, demand visibility from large enterprise contracts provides a long-term revenue foundation. Even if utilization fluctuates, contracted capacity ensures baseline demand.

Second, early unit economics in the AI cloud segment suggest improving scalability. As infrastructure fills and utilization increases, margins in high-performance compute workloads tend to expand due to fixed-cost absorption.

Third, strategic alignment with NVIDIA enhances supply chain access, potentially giving Nebius priority allocation for next-generation GPUs. In a constrained supply environment, this advantage can translate into faster deployment cycles and higher revenue capture.

From this perspective, Nebius represents a rare opportunity to invest in the physical backbone of AI growth, rather than software-layer applications that may face faster commoditization cycles.

The Bear Case: Capital Intensity and Structural Risk

Despite strong growth, skeptics highlight significant structural risks associated with Nebius’ model. The most immediate concern is capital intensity. With projected CapEx potentially reaching tens of billions of dollars, the company must continuously finance large-scale infrastructure before revenue fully materializes from deployed assets.

This creates a timing mismatch between spending and cash flow generation, which can pressure profitability and increase dilution risk over time.

Another key concern is depreciation. AI hardware cycles are shortening, meaning that GPUs and related infrastructure may lose value faster than traditional data center assets. This creates recurring write-down pressure and limits long-term margin expansion.

Customer concentration also remains a structural vulnerability. A significant portion of Nebius’ demand is tied to a small number of hyperscaler clients. If these customers shift workloads in-house or optimize their own AI chips, external demand could flatten or become more volatile.

Finally, the long-term threat of hyperscaler vertical integration cannot be ignored. Companies like Meta and Microsoft continue to develop proprietary AI silicon, which could reduce reliance on third-party GPU clouds over time, even if not eliminating it entirely.

Strategic Outlook: Execution Becomes the Deciding Factor

The core investment debate around Nebius has now shifted from survival to execution. The company has secured capital, demand visibility, and strategic positioning within the AI ecosystem. The remaining challenge is operational: delivering gigawatt-scale infrastructure on time, at cost, and at utilization rates that justify the capital deployed.

In the near term, investors are likely to focus less on headline revenue growth and more on utilization rates, contract longevity, and deployment efficiency. These metrics will determine whether Nebius evolves into a durable AI infrastructure utility or remains a high-growth but capital-intensive scaling platform.

Ultimately, Nebius represents a high-conviction structural bet on the continued expansion of global AI compute demand. However, it is also a business where execution risk remains elevated, and where small deviations in infrastructure timelines or demand cycles can have outsized financial impacts.

In this sense, Nebius is not simply a growth story—it is a test of whether large-scale AI infrastructure can be built fast enough to meet the accelerating demands of the artificial intelligence economy.