Investing in Stocks and ETFs: Explaining Each Strategy

Many people view the stock market as a complex, intimidating puzzle. In reality, you build your wealth on a very simple concept: whether investing in individual stocks or buying a basket of assets via ETFs, you buy a piece of a business so you can get paid a share of its profits. Over time, investors have developed different methods to collect these profits. They routinely move from buying single companies to using advanced, high-yield funds that can turn a $110,000 investment into a $1,300 tax-free monthly paycheck.

To execute this modern strategy successfully, you must understand how traditional investing evolved, how funds simplify the process, and how you can utilize compounding to create an unstoppable snowball of wealth.

The Traditional Way: Buying Individual Stocks

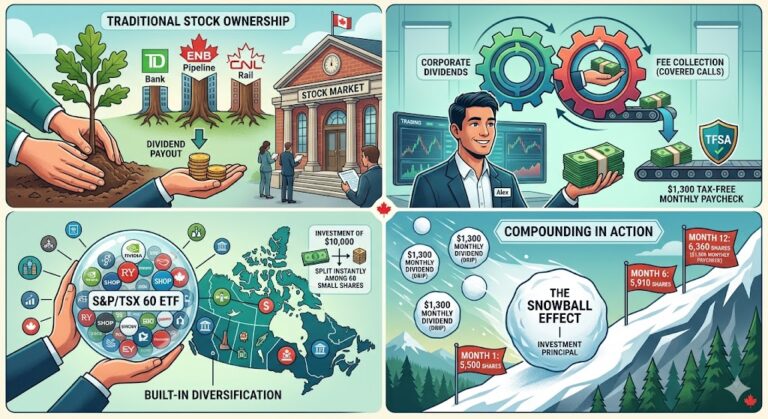

Imagine you want to invest directly in the Canadian economy. You decide to buy shares of iconic individual companies that you see every day, such as TD Bank, Enbridge, or Canadian National Railway. While purchasing individual stocks gives you direct ownership in those specific businesses, many investors prefer to bundle these Canadian giants together using Canadian equity ETFs. By choosing ETFs over single stock selection, you can gain instant exposure to the entire Canadian market in a single transaction.

When you purchase an individual stock, you become a literal part-owner of that specific corporation. As a part-owner, you stand to make money in two distinct ways:

-

Capital Growth: If the company invents new products, gains more customers, and grows its profits, the market drives the value of your stock up. Consequently, you can sell your share later to another investor for a profit.

-

Dividends: Real wealth-building happens through dividends. When a stable company makes a profit at the end of a business quarter, it does not keep all the cash. Instead, it sends a portion of those profits directly back to you and other shareholders as a cash reward. This cash payout is your dividend.

The Big Problem: Buying individual stocks requires an immense amount of your personal time, deep research, and endless financial homework. Furthermore, it exposes you to high concentration risk. If you put all your savings into just one or two companies, and those specific businesses face a major crisis, a lawsuit, or bankruptcy, you could lose a massive portion of your life savings overnight.

The Modern Solution: Understanding ETF Basics

To solve the risk and high cost of tracking down individual companies, the financial world created a modern tool called an ETF (Exchange-Traded Fund).

An ETF acts as a single financial asset that automatically holds a pre-packaged group of multiple individual stocks. Instead of spending your money to buy 100% of a single company like Nvidia, you buy one share of an ETF. That single purchase instantly gives you a specific, proportional percentage of hundreds of different corporations simultaneously. By utilizing ETFs, investors can instantly diversify their portfolios without having to manage dozens of separate positions, making ETFs one of the most efficient tools for long-term wealth building.

For example, a standard tech ETF might allocate 7% of your money to Nvidia, 7% to Microsoft, 6% to Apple, and split the remaining balance across dozens of other major firms.

-

Proportional Ownership: When you invest in an ETF, the fund automatically distributes your money across an entire corporate sector based on these exact target percentages.

-

Built-In Diversification: Because the fund spreads your capital thin across multiple individual stocks as a collective group, you completely insulate yourself from a single company crashing. If Nvidia experiences a severe structural drop on the stock market, it only impacts a tiny fraction of your overall investment, while the other corporate stocks in the group maintain your stability.

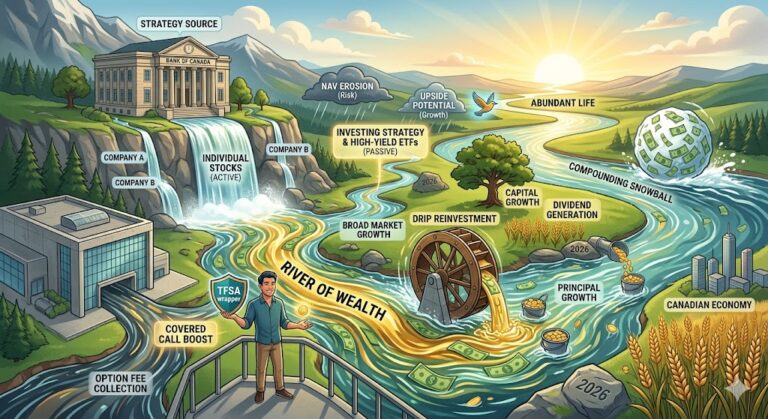

The High-Yield Strategy: How Investors Maximize Dividends

Most standard ETFs pay a modest dividend of around 2% to 4% per year, usually distributing that cash to your account every three months. Because these traditional ETFs focus primarily on long-term capital growth, their immediate cash distributions remain relatively low. However, a specialized group of income-focused investors rejects this slow timeline. They want maximum monthly cash flow from high-yield ETFs rather than waiting decades for individual stock prices to rise.

To see how this works, consider an investor named Alex who has $110,000 sitting in cash. Alex does not want to buy standard growth stocks; instead, Alex’s primary goal is to generate immediate cash to supplement daily living expenses.

Alex opens a self-directed online brokerage account, transfers the $110,000 into a Tax-Free Savings Account (TFSA) wrapper, and logs into the trading platform. Alex searches for a specialized Canadian “Covered Call” ETF trading at $20 per share and places a limit order to purchase exactly 5,500 shares. By deploying the full $110,000 into this specific fund, Alex activates two powerful financial boosts:

Boost 1: The “Fee-Collection” Trick

The ETF Alex purchased does not just sit around waiting for regular company dividends to trickle in. Instead, the fund manager plays a clever game by selling a type of “insurance contract” (called a covered call option) to aggressive, speculative stock traders in the market.

Those traders pay the ETF massive upfront fees for these contracts. The fund manager takes all those collected fees, packages them together with the regular corporate dividends, and passes them directly to Alex. Because the fund generates income from both corporate profits and trading fees, it yields an incredible 14% annually—meaning Alex receives roughly $1,300 deposited directly into their brokerage account every single month.

Boost 2: The Ultimate Tax Shield

Because Alex bought these 5,500 shares inside a TFSA, the account acts as a protective shield. Normally, if you make $1,300 a month in extra income, the government treats it like a second job and takes a large chunk of it in income taxes. But inside the TFSA, the government cannot tax a single penny of Alex’s monthly payout. It remains 100% tax-free spending money.

The Snowball Effect: How Compounding Automatically Grows the Payout

A common question people ask when looking at this strategy is: Does that $1,300 monthly payout stay the same forever, or does it eventually shrink?

In reality, smart investors watch their monthly payouts go up over time, not down. They do this by harnessing the mathematical power of compounding. Instead of taking the $1,300 cash out of the account to spend it, the investor leaves the dividend money completely alone. They set up their brokerage account to automatically buy more shares of the exact same ETF the very day the cash arrives.

This process is called a DRIP (Dividend Reinvestment Plan), and it triggers an explosive financial snowball effect:

-

Month 1: The investor starts with 5,500 shares. The ETF pays out its dividend, and $1,300 cash hits the account. The system instantly uses that $1,300 to buy 65 brand-new shares for free (assuming a $20 stock price). The investor now owns 5,565 shares.

-

Month 2: Because the investor left the dividend to buy more shares, they now get paid a dividend on 5,565 shares instead of 5,550. Their monthly payout automatically increases to $1,315. The system takes that $1,315 and buys roughly 66 more shares.

-

Month 12: After a full year of leaving the dividends to buy more shares, the investor owns hundreds of extra shares without ever adding a single extra penny of their own savings. Their monthly check has naturally compounded and snowballed into $1,500 or more.

This is how compounding works in real time: your money makes dividend money, and then that dividend money buys new shares to make even more dividend money. Additionally, because the fund’s fee-collection trick relies on stock market drama, the fund manager collects more fee money when the market is wild and rocky. This means the investor’s monthly check can physically increase during periods of market chaos, providing even more cash fuel to accelerate the compounding snowball.

The Fundamental Trade-Off: Income vs. Long-Term Growth

Before you adopt this strategy, you must understand one vital trade-off. Think of this approach like buying a physical rental property. You collect $1,300 a month in rent cash flow, but the resale value of the house itself will still fluctuate based on the local housing market.

By choosing these specialized ETFs, you are explicitly prioritizing maximum immediate monthly income over long-term price growth. However, this high-yield engine comes with two distinct catches that you cannot afford to ignore.

First, you sacrifice your upside potential. When individual stocks skyrocket, the option contracts your fund manager sold force the ETF to sell its winning shares early. As a result, your fund misses out on massive market rallies. While a standard growth stock might surge 20% in a bull market, your high-yield ETF will likely experience only a fraction of that growth.

Second, you face the risk of principal erosion. Because these funds capture the full brunt of market crashes but cap your gains during market recoveries, the underlying value of your investment can slowly shrink over time. In the financial world, experts call this Net Asset Value (NAV) decay.

Consequently, your original $110,000 investment will not just fluctuate; it may actually decrease on paper over a multi-year period if you spend the cash instead of turning on the snowball effect.

Ultimately, this strategy transforms your portfolio into a specialized income machine. Your tax-free monthly paycheck will keep rolling into your account, but you must consistently reinvest those dividends through a DRIP to defend your principal against market downturns and keep your financial momentum rolling.